Fenchurch Law announces Singapore expansion plans

Fenchurch Law, the UK’s leading firm working exclusively for insurance policyholders and brokers, plans to offer its specialist legal support outside of the UK for the first time, announcing plans…

News

This is the place to find out what we’re thinking as we think it. It’s an eclectic and often opinionated mix of content, including news, articles on case law and recent legislation, and webinars. We’re keen to ensure our content is of interest and value to our existing and prospective clients, so please do get in touch and let us know what you think of individual pieces, or our communication programme more generally.

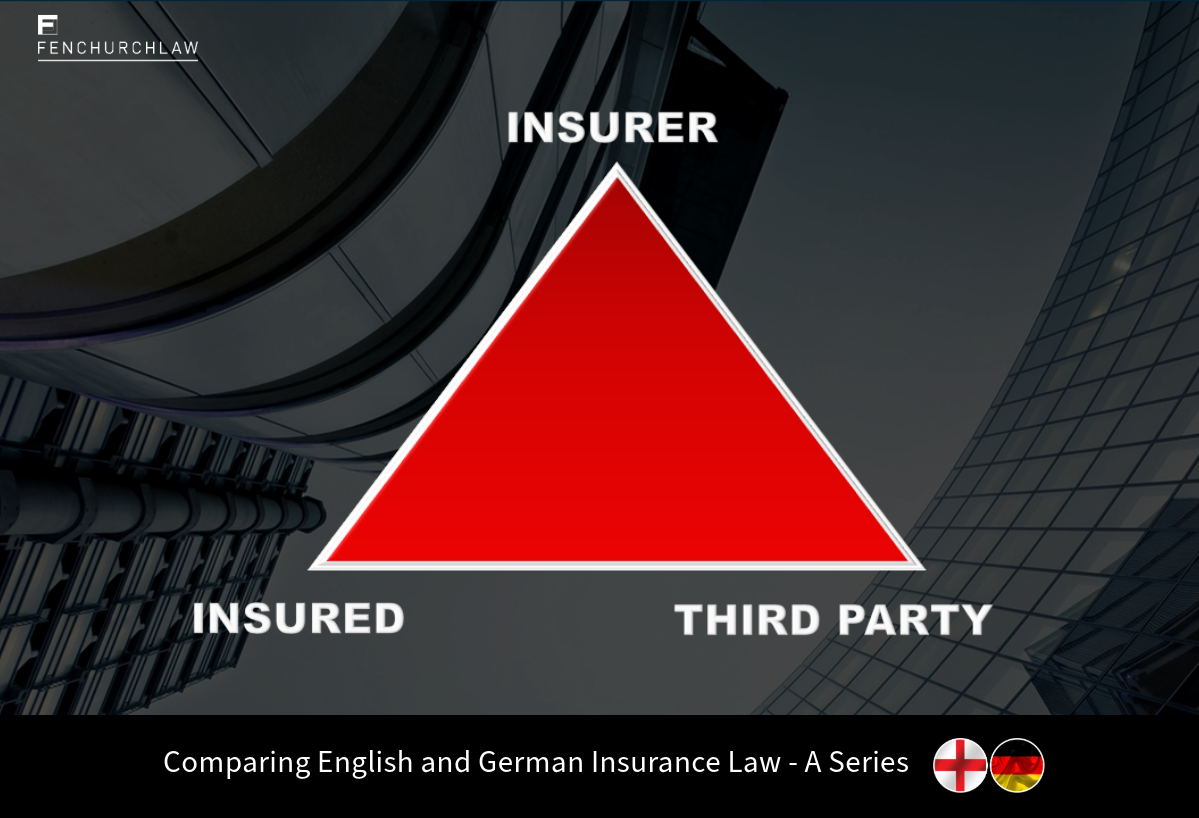

Comparing English and German Insurance Law – Part 2: A Third Party’s Right to Claim Directly Against Insurers

10 April 2024

By Isabel Becker

Insurers have deep pockets, while the average person on the street is incapable of paying claims for significant damages. That […]

What is unfairly prejudicial conduct entitling a shareholder to relief from the Court – and are such claims indemnified under the company’s D&O Policy?

8 April 2024

By Fenchurch Law

Successive versions of the Companies Act (most recently Section 994 of the 2006 Act (“CA 2006”)) have provided protection and […]

The Good, the Bad & the Ugly: #23 (the Good): Scotbeef Limited v D&S Storage Limited (In Liquidation) Lonham Group Limited [2024]

5 April 2024

By Chloe Franklin

Welcome to the latest in the series of blogs from Fenchurch Law: 100 cases every policyholder needs to know. An […]

Webinar – Too Hot to Handle – a cautionary tale about Hot Works Conditions

By Alex Rosenfield

Agenda Hot Works Conditions are a staple of contractors’ public liability policies. They require certain precautions to be taken before, […]

Fenchurch Law hands decision making power to its people, announcing shift to employee ownership model

27 March 2024

By Michael Hayes

Fenchurch Law, the UK’s leading firm working exclusively for policyholders and brokers on complex insurance disputes, has announced that 60% […]

Pallister Limited v (1) Fate Limited (in liquidation) (2) The National Insurance and Guarantee Corporation Limited (3) UK Insurance Limited

12 February 2019

By Michael Hayes

In this recent decision in the Queen’s Bench Division, the court examined the meaning of “property belonging to” in the […]

Avoid getting out of your depth with notifications – the Court considers the scope of notification in Euro Pools plc v Royal & Sun Alliance Insurance plc

22 February 2018

By Michael Hayes

In Euro Pools Plc v Royal & Sun Alliance Insurance Plc[1] the Court considered (amongst other things) the scope of […]

Bluebon Ltd (in liquidation) – v – (1) Ageas (UK) Ltd (2) Aviva Insurance Ltd (3) Towergate Underwriting Group Ltd (2017)

22 January 2018

By Michael Hayes

What was the proper construction of an electrical installation inspection warranty? Bluebon Limited (‘Bluebon’) brought proceedings against their insurers, Ageas […]

Dalecroft Properties Limited – v – Underwriters

27 June 2017

By Michael Hayes

Dalecroft Properties Limited – v – Underwriters subscribing to Certificate Number 755/BA004/2008/OIS/00000282/2008/005 [2017] EWHC 1263 (Comm) This recent decision by […]

“One event or two?” What is the proper construction of the phrase “arising from one event” within the aggregation clause in a reinsurance contract?

1 November 2016

By Michael Hayes

Re MIC Simmonds v. AJ Gammell The commercial court upheld an arbitration award and concluded that the arbitrators had correctly […]

The ordinary measure of indemnity: Great Lakes Reinsurance (UK) SE v Western Trading Limited

13 October 2016

By Michael Hayes

In the latest in a series of pro-policyholder decisions by the courts, the Court of Appeal yesterday handed down a […]

AIG Europe Limited –v- OC320301 LLP and Others

20 August 2015

By Michael Hayes

While some in the market may regard the recent decision of AIG Europe Limited -v- OC320301 LLP [2015] EWHC 2398 […]

Has the Enterprise Act Expanded the Duty of Fair Presentation?

13 October 2017

By Michael Hayes

For more than a century after the Marine Insurance Act of 1906, the law relating to insurance contracts was a […]

Insurance Act 2015: Some Insurers Crying Foul

9 February 2017

By Michael Hayes

When the Insurance Act 2015 came into force in August 2016, it was hailed as the biggest reform of this […]

Third Parties (Rights Against Insurers) Act 2010

26 April 2010

By Michael Hayes

The Third Parties (Rights Against Insurers) Act 2010 which received Royal Assent on 25.03.2010 has amended previous legislation governing the […]

Financial Services Act 2010 – class actions removed

By Michael Hayes

The Financial Services Act 2010 received Royal Assent on 08.04.2010, being amongst the last few pieces of legislation rushed through […]

Financial Services Bill progress

16 February 2010

By Michael Hayes

The Financial Services Bill is due to receive its second reading in the House of Lords (when all aspects of […]

Fenchurch Law announces Singapore expansion plans

15 April 2024

By Michael Hayes

Fenchurch Law, the UK’s leading firm working exclusively for insurance policyholders and brokers, plans to offer its specialist legal support […]

Fenchurch Law hands decision making power to its people, announcing shift to employee ownership model

27 March 2024

By Michael Hayes

Fenchurch Law, the UK’s leading firm working exclusively for policyholders and brokers on complex insurance disputes, has announced that 60% […]

Fenchurch Law bolsters insurance disputes team in London with new hires

22 January 2024

By Michael Hayes

Fenchurch Law has announced the expansion of its coverage disputes team in London with two new hires; Jessica Chappell and […]

Fenchurch Law’s Chiltern 50 Charity Walk

22 August 2023

By Michael Hayes

On the 23rd of September 2023, employees of Fenchurch Law will be taking on the challenge of the Chiltern 50. […]

Fenchurch Law bolsters insurance disputes team in London with three new hires

15 December 2022

By Michael Hayes

Fenchurch Law, the UK’s leading firm working exclusively for policyholders and brokers on complex insurance disputes, has announced the expansion […]

Fenchurch Law boosts insurance disputes team with double hire

18 August 2022

By Michael Hayes

Fenchurch Law, the UK’s leading firm working exclusively for policyholders and brokers on complex insurance disputes, has announced the expansion […]

Fenchurch Law launches new Reinsurance and International Risks practice

1 February 2022

By Michael Hayes

Fenchurch Law, the leading UK legal firm working exclusively for policyholders and brokers on insurance coverage disputes, has launched a […]

Fenchurch Law expands property coverage disputes team

18 February 2020

By Michael Hayes

Fenchurch Law, the leading UK firm working exclusively for policyholders and brokers on complex insurance disputes, has appointed Nicola Bowen […]

Fenchurch Law expands coverage dispute team with Le Marquer appointment

8 January 2020

By Michael Hayes

Fenchurch Law, the leading UK firm working exclusively for policyholders and brokers on complex insurance disputes, has appointed Aaron Le […]

Fenchurch Law launches “The Associate Series”

11 October 2019

By Michael Hayes

Fenchurch Law’s new initiative, The Associate Series, is being launched with a view to sharing our knowledge and experience of […]

Fenchurch Law adds Goodship to Construction Risks team

19 September 2019

By Michael Hayes

Fenchurch Law, the leading UK firm working exclusively for policyholders and brokers on complex insurance disputes, has appointed Rob Goodship […]

Fenchurch Law expands coverage dispute team with triple hire

8 November 2018

By Michael Hayes

Fenchurch Law, the leading UK firm working exclusively for policyholders and brokers on complex insurance disputes, has made a trio […]

Fenchurch Law awarded Investor In Customers “Gold” Award for client experience

23 October 2018

By Michael Hayes

Fenchurch Law, the UK’s leading firm of policyholder-focused insurance dispute lawyers, have achieved a ‘gold’ award from the independent Investor […]

Fenchurch Law recognised for claims dispute expertise with tier one ranking in Legal 500

23 October 2017

By Michael Hayes

Fenchurch Law, the leading UK firm working exclusively for policyholders and brokers on complex insurance disputes, has received a tier […]

Fenchurch Law continues expansion of insurance claims disputes capability with Hunter appointment

19 July 2017

By Michael Hayes

Fenchurch Law, the leading UK firm working exclusively for policyholders and brokers on complex insurance disputes, has further expanded its […]

Fenchurch Law strengthens professions insurance disputes capabilities with Rosenfield hire

19 May 2017

By Michael Hayes

Fenchurch Law, the UK’s leading firm working exclusively for policyholders and brokers on complex insurance disputes, has announced the appointment […]

Fenchurch Law appoints Morris to strengthen financial lines insurance disputes team

3 February 2017

By Michael Hayes

Fenchurch Law, the UK’s leading firm working exclusively for policyholders and brokers on complex insurance disputes, announces the appointment of […]

Fenchurch Law boosts insurance disputes team with three new appointments

13 September 2016

By Michael Hayes

Fenchurch Law, the UK’s leading firm working exclusively for policyholders and brokers on complex insurance disputes, announces the expansion of […]

Fenchurch Law launches combined legal service and costs cover for policyholders with insurance claims disputes

28 July 2016

By Michael Hayes

Fenchurch Law, the UK’s leading firm working exclusively for policyholders and brokers on complex insurance disputes, has launched Fenchurch Law […]

Fenchurch Law: Insurance Law Firm of the Year

3 June 2016

By Michael Hayes

Fenchurch Law won the award for Insurance Law Firm of the Year at the 6th Post Magazine Claims Awards held […]

Fenchurch Law trainee to qualify

2 June 2016

By Michael Hayes

Fenchurch Law, one of the UK’s leading firms working exclusively for policyholders and brokers on complex insurance disputes are delighted […]

Fenchurch Law boosts professions practice with associate appointment

3 May 2016

By Michael Hayes

Fenchurch Law, one of the UK’s leading firms working exclusively for policyholders and brokers on complex insurance disputes, has expanded […]

Fenchurch Law Ltd shortlisted for Insurance Law Firm of the Year Award

12 April 2016

By Michael Hayes

Fenchurch Law Ltd has been shortlisted for the second time for the Insurance Law Firm of the Year in the […]

Construction and Professional Indemnity expert Amy Lacey joins Fenchurch Law

7 March 2016

By Michael Hayes

Insurance coverage specialists, Fenchurch Law, have announced that Amy Lacey has joined as a partner from Rosling King. Amy will […]

Fenchurch Law Ltd Move to 40 Lime Street

2 February 2016

By Michael Hayes

Please note that from Monday 1st February 2016 Fenchurch Law Ltd will have a new home in the heart of […]

Fenchurch Law Grows its Expertise with Insurance Litigation Specialist Hire

15 October 2015

By Michael Hayes

Insurance coverage specialists, Fenchurch Law, have announced that John Curran has joined as a partner. John will concentrate on insurance […]

Fenchurch Law moves up Legal 500 Rankings

18 September 2015

By Michael Hayes

The new Legal 500 rankings have been published and we are pleased to announce that Fenchurch Law has moved up […]

Insurance Coverage Partner joins Fenchurch Law

16 July 2015

By Michael Hayes

Insurance coverage specialists, Fenchurch Law, have today announced that Jonathan Corman has joined as a partner. Jonathan has been an […]

Fenchurch Law promotes Daniel Brooks to Associate Partner

7 May 2015

By Michael Hayes

Fenchurch Law, the policyholder-focused coverage specialists, have promoted Daniel Brooks to Associate Partner. Daniel joined Fenchurch Law in 2014 and […]

Fenchurch Law Ltd shortlisted for Insurance Law Firm of the Year Award.

15 April 2015

By Michael Hayes

Fenchurch Law Ltd has been shortlisted for the Insurance Law Firm of the Year in the prestigious Claims Awards 2015, […]

Claims for compensation under the Riot (Damages) Act 1886

7 September 2011

By Michael Hayes

The Riot (Damages) Act 1886 is designed to compensate people and businesses which suffer losses following riots. It also enables […]

Our comments on film finance schemes for the Financial Times

8 March 2010

By Michael Hayes

Film finance schemes are back in the news for the wrong reasons, with HMRC investigating claims for tax relief by […]

The Good, the Bad & the Ugly: #23 (the Good): Scotbeef Limited v D&S Storage Limited (In Liquidation) Lonham Group Limited [2024]

5 April 2024

By Chloe Franklin

Welcome to the latest in the series of blogs from Fenchurch Law: 100 cases every policyholder needs to know. An […]

The Good, the Bad & the Ugly: #22 (The Ugly) MacPhail v Allianz Insurance plc [2023] EWHC 1035 (Ch)

24 August 2023

By Chloe Franklin

Welcome to the latest in the series of blogs from Fenchurch Law: 100 cases every policyholder needs to know. An […]

The Good, the Bad & the Ugly: #21 (the Good). Pan Atlantic Insurance Co Ltd v Pine Top Insurance Co Ltd

23 August 2023

By Grace Williams

Welcome to the latest in the series of blogs from Fenchurch Law: 100 cases every policyholder needs to know. An […]

The Good, the Bad & the Ugly: #20 (The Good) Brian Leighton (Garages) Limited v Allianz Insurance Plc

17 February 2023

By Grace Williams

Welcome to the latest in the series of blogs from Fenchurch Law: 100 cases every policyholder needs to know. An […]

The Good, the Bad & the Ugly: #19 (The Ugly). Rashid v Direct Savings

12 December 2022

By Toby Nabarro

Welcome to the latest in the series of blogs from Fenchurch Law: 100 cases every policyholder needs to know. An […]

The Good, the Bad & the Ugly: #18 (The Good). Carter v Boehm (1766)

31 October 2022

By Dru Corfield

Welcome to the latest in the series of blogs from Fenchurch Law: 100 cases every policyholder needs to know. An […]

The Good, the Bad & the Ugly: 100 cases every policyholder needs to know. #17 (The Ugly). Diab v. Regent Insurance Company

28 March 2022

By Serena Mills

Welcome to the latest in the series of blogs from Fenchurch Law: 100 cases every policyholder needs to know. An opinionated and […]

The Good, the Bad & the Ugly: 100 cases every policyholder needs to know. #16 (The Good). Technology Holdings Ltd v IAG New Zealand Ltd [2008]

By Rob Goodship

Welcome to the latest in the series of blogs from Fenchurch Law: 100 cases every policyholder needs to know. An opinionated and […]

The Good, the Bad & the Ugly: #15 (The Good & Bad). West Wake Price & Co v Ching

20 September 2021

By Jonathan Corman & Toby Nabarro

Welcome to the latest in the series of blogs from Fenchurch Law: 100 cases every policyholder needs to know. An opinionated and […]

The Good, the Bad & the Ugly: 100 cases every policyholder needs to know. #14 (The Good & Ugly). Arch Insurance (UK) Ltd v FCA and others

14 June 2021

By Rob Goodship

Welcome to the latest in the series of blogs from Fenchurch Law: 100 cases every policyholder needs to know. An opinionated and […]

The Good, the Bad & the Ugly: #13 (The Bad). Haberdashers’ Aske’s Federation Trust & v Lakehouse Contracts

17 March 2021

By Amy Lacey

Welcome to the latest in the series of blogs from Fenchurch Law: 100 cases every policyholder needs to know. An […]

The Good, the Bad & the Ugly: 100 cases every policyholder needs to know. #12 (The Ugly). Tesco Stores Ltd v Constable & Ors

12 February 2021

By Rob Goodship & Toby Nabarro

Welcome to the latest in the series of blogs from Fenchurch Law: 100 cases every policyholder needs to know. An […]

The Good, the Bad & the Ugly: 100 cases every policyholder needs to know. #11 (The Good). R&R Developments v AXA

14 December 2020

By Alex Rosenfield

Welcome to the latest in the series of blogs from Fenchurch Law: 100 cases every policyholder needs to know. An […]

The Good, the Bad & the Ugly: 100 cases every policyholder needs to know. #10 (The Bad). Orient-Express Hotels v Generali

29 September 2020

By Fenchurch Law

Welcome to the latest in the series of blogs from Fenchurch Law: 100 cases every policyholder needs to know. An opinionated […]

The Good, the Bad & the Ugly: 100 cases every policyholder needs to know. #9 (The Good). UK Acorn Finance Ltd v Markel (UK) Ltd

17 June 2020

By Fenchurch Law

Welcome to the latest in the series of blogs from Fenchurch Law: 100 Cases Every Policyholder Needs to Know. An […]

The Good, the Bad & the Ugly: 100 cases every policyholder needs to know. #8 (The Good). Thornton Springer v NEM Insurance Co Limited

27 February 2020

By Daniel Robin

Welcome to the latest in the series of blogs from Fenchurch Law: 100 Cases Every Policyholder Needs to Know. An […]

The Good, the Bad & the Ugly: 100 cases every policyholder needs to know. #7 (The Good). Woodford and Hillman -v- AIG

9 September 2019

By Michael Hayes

Welcome to the latest in the series of blogs from Fenchurch Law: 100 cases every policyholder needs to know. An opinionated […]

The Good, the Bad & the Ugly: 100 cases every policyholder needs to know. #6 (The Bad). Orient-Express Hotels v Generali

1 July 2019

By Michael Hayes

Welcome to the latest in the series of blogs from Fenchurch Law: 100 cases every policyholder needs to know. An […]

The Good, the Bad & the Ugly: 100 cases every policyholder needs to know. #5 (The Ugly). AIG v Woodman

20 December 2018

By Michael Hayes

Welcome to the latest in the series of blogs from Fenchurch Law: 100 cases every policyholder needs to know. An […]

The Good, the Bad & the Ugly: 100 cases every policyholder needs to know. #4 (The Good). The Orjula

9 November 2018

By Amy Lacey

Welcome to the latest in the series of blogs from Fenchurch Law: 100 cases every policyholder needs to know. An […]

The Good, the Bad & the Ugly: 100 cases every policyholder needs to know. #3 (The Ugly). Pioneer Concrete

27 February 2018

By Michael Hayes

Welcome to the latest in the series of blogs from Fenchurch Law: 100 cases every policyholder needs to know. An […]

The Good, the Bad & the Ugly: 100 cases every policyholder needs to know. #2 (The Ugly). Kosmar Villa Holidays plc

21 July 2017

By Michael Hayes

Welcome to the latest in the series of blogs from Fenchurch Law: 100 cases every policyholder needs to know. An […]

The Good, the Bad & the Ugly: 100 cases every policyholder needs to know. #1 (The Bad). Why Wayne Tank is wrongly decided.

11 April 2017

By Amy Lacey

Welcome to a new series of blogs from Fenchurch Law: 100 cases every policyholder needs to know. An opinionated and […]

Fenchurch Law announces Singapore expansion plans

15 April 2024

Michael Hayes

Fenchurch Law, the UK’s leading firm working exclusively for insurance policyholders and brokers, plans to offer its specialist legal support […]

What is unfairly prejudicial conduct entitling a shareholder to relief from the Court – and are such claims indemnified under the company’s D&O Policy?

8 April 2024

Fenchurch Law

Successive versions of the Companies Act (most recently Section 994 of the 2006 Act (“CA 2006”)) have provided protection and […]

Fenchurch Law hands decision making power to its people, announcing shift to employee ownership model

27 March 2024

Michael Hayes

Fenchurch Law, the UK’s leading firm working exclusively for policyholders and brokers on complex insurance disputes, has announced that 60% […]

Fenchurch Law bolsters insurance disputes team in London with new hires

22 January 2024

Michael Hayes

Fenchurch Law has announced the expansion of its coverage disputes team in London with two new hires; Jessica Chappell and […]

Fenchurch Law’s Chiltern 50 Charity Walk

22 August 2023

Michael Hayes

On the 23rd of September 2023, employees of Fenchurch Law will be taking on the challenge of the Chiltern 50. […]

Fenchurch Law bolsters insurance disputes team in London with three new hires

15 December 2022

Michael Hayes

Fenchurch Law, the UK’s leading firm working exclusively for policyholders and brokers on complex insurance disputes, has announced the expansion […]

Fenchurch Law boosts insurance disputes team with double hire

18 August 2022

Michael Hayes

Fenchurch Law, the UK’s leading firm working exclusively for policyholders and brokers on complex insurance disputes, has announced the expansion […]

Fenchurch Law launches new Reinsurance and International Risks practice

1 February 2022

Michael Hayes

Fenchurch Law, the leading UK legal firm working exclusively for policyholders and brokers on insurance coverage disputes, has launched a […]

Fenchurch Law expands property coverage disputes team

18 February 2020

Michael Hayes

Fenchurch Law, the leading UK firm working exclusively for policyholders and brokers on complex insurance disputes, has appointed Nicola Bowen […]

Fenchurch Law expands coverage dispute team with Le Marquer appointment

8 January 2020

Michael Hayes

Fenchurch Law, the leading UK firm working exclusively for policyholders and brokers on complex insurance disputes, has appointed Aaron Le […]

Fenchurch Law launches “The Associate Series”

11 October 2019

Michael Hayes

Fenchurch Law’s new initiative, The Associate Series, is being launched with a view to sharing our knowledge and experience of […]

Fenchurch Law adds Goodship to Construction Risks team

19 September 2019

Michael Hayes

Fenchurch Law, the leading UK firm working exclusively for policyholders and brokers on complex insurance disputes, has appointed Rob Goodship […]

PII: What happened in 2018?

21 February 2019

Michael Hayes

A number of interesting cases relating to professional indemnity insurance passed through the courts in 2018, and this article looks […]

Pallister Limited v (1) Fate Limited (in liquidation) (2) The National Insurance and Guarantee Corporation Limited (3) UK Insurance Limited

12 February 2019

Michael Hayes

In this recent decision in the Queen’s Bench Division, the court examined the meaning of “property belonging to” in the […]

Fenchurch Law expands coverage dispute team with triple hire

8 November 2018

Michael Hayes

Fenchurch Law, the leading UK firm working exclusively for policyholders and brokers on complex insurance disputes, has made a trio […]

Fenchurch Law awarded Investor In Customers “Gold” Award for client experience

23 October 2018

Michael Hayes

Fenchurch Law, the UK’s leading firm of policyholder-focused insurance dispute lawyers, have achieved a ‘gold’ award from the independent Investor […]

Avoid getting out of your depth with notifications – the Court considers the scope of notification in Euro Pools plc v Royal & Sun Alliance Insurance plc

22 February 2018

Michael Hayes

In Euro Pools Plc v Royal & Sun Alliance Insurance Plc[1] the Court considered (amongst other things) the scope of […]

Bluebon Ltd (in liquidation) – v – (1) Ageas (UK) Ltd (2) Aviva Insurance Ltd (3) Towergate Underwriting Group Ltd (2017)

Michael Hayes

What was the proper construction of an electrical installation inspection warranty? Bluebon Limited (‘Bluebon’) brought proceedings against their insurers, Ageas […]

Fenchurch Law recognised for claims dispute expertise with tier one ranking in Legal 500

23 October 2017

Michael Hayes

Fenchurch Law, the leading UK firm working exclusively for policyholders and brokers on complex insurance disputes, has received a tier […]

Has the Enterprise Act Expanded the Duty of Fair Presentation?

13 October 2017

Michael Hayes

For more than a century after the Marine Insurance Act of 1906, the law relating to insurance contracts was a […]

Fenchurch Law continues expansion of insurance claims disputes capability with Hunter appointment

19 July 2017

Michael Hayes

Fenchurch Law, the leading UK firm working exclusively for policyholders and brokers on complex insurance disputes, has further expanded its […]

Dalecroft Properties Limited – v – Underwriters

27 June 2017

Michael Hayes

Dalecroft Properties Limited – v – Underwriters subscribing to Certificate Number 755/BA004/2008/OIS/00000282/2008/005 [2017] EWHC 1263 (Comm) This recent decision by […]

Fenchurch Law strengthens professions insurance disputes capabilities with Rosenfield hire

Michael Hayes

Fenchurch Law, the UK’s leading firm working exclusively for policyholders and brokers on complex insurance disputes, has announced the appointment […]

Insurance Act 2015: Some Insurers Crying Foul

9 February 2017

Michael Hayes

When the Insurance Act 2015 came into force in August 2016, it was hailed as the biggest reform of this […]

Fenchurch Law appoints Morris to strengthen financial lines insurance disputes team

3 February 2017

Michael Hayes

Fenchurch Law, the UK’s leading firm working exclusively for policyholders and brokers on complex insurance disputes, announces the appointment of […]

Fenchurch Law boosts insurance disputes team with three new appointments

13 September 2016

Michael Hayes

Fenchurch Law, the UK’s leading firm working exclusively for policyholders and brokers on complex insurance disputes, announces the expansion of […]

Fenchurch Law launches combined legal service and costs cover for policyholders with insurance claims disputes

28 July 2016

Michael Hayes

Fenchurch Law, the UK’s leading firm working exclusively for policyholders and brokers on complex insurance disputes, has launched Fenchurch Law […]

Fenchurch Law: Insurance Law Firm of the Year

3 June 2016

Michael Hayes

Fenchurch Law won the award for Insurance Law Firm of the Year at the 6th Post Magazine Claims Awards held […]

Fenchurch Law trainee to qualify

2 June 2016

Michael Hayes

Fenchurch Law, one of the UK’s leading firms working exclusively for policyholders and brokers on complex insurance disputes are delighted […]

Fenchurch Law boosts professions practice with associate appointment

3 May 2016

Michael Hayes

Fenchurch Law, one of the UK’s leading firms working exclusively for policyholders and brokers on complex insurance disputes, has expanded […]

Fenchurch Law Ltd shortlisted for Insurance Law Firm of the Year Award

12 April 2016

Michael Hayes

Fenchurch Law Ltd has been shortlisted for the second time for the Insurance Law Firm of the Year in the […]

Construction and Professional Indemnity expert Amy Lacey joins Fenchurch Law

7 March 2016

Michael Hayes

Insurance coverage specialists, Fenchurch Law, have announced that Amy Lacey has joined as a partner from Rosling King. Amy will […]

Fenchurch Law Ltd Move to 40 Lime Street

2 February 2016

Michael Hayes

Please note that from Monday 1st February 2016 Fenchurch Law Ltd will have a new home in the heart of […]

Fenchurch Law Grows its Expertise with Insurance Litigation Specialist Hire

15 October 2015

Michael Hayes

Insurance coverage specialists, Fenchurch Law, have announced that John Curran has joined as a partner. John will concentrate on insurance […]

Fenchurch Law moves up Legal 500 Rankings

18 September 2015

Michael Hayes

The new Legal 500 rankings have been published and we are pleased to announce that Fenchurch Law has moved up […]

Insurance Coverage Partner joins Fenchurch Law

16 July 2015

Michael Hayes

Insurance coverage specialists, Fenchurch Law, have today announced that Jonathan Corman has joined as a partner. Jonathan has been an […]

Fenchurch Law promotes Daniel Brooks to Associate Partner

7 May 2015

Michael Hayes

Fenchurch Law, the policyholder-focused coverage specialists, have promoted Daniel Brooks to Associate Partner. Daniel joined Fenchurch Law in 2014 and […]

Fenchurch Law Ltd shortlisted for Insurance Law Firm of the Year Award.

15 April 2015

Michael Hayes

Fenchurch Law Ltd has been shortlisted for the Insurance Law Firm of the Year in the prestigious Claims Awards 2015, […]

Claims for compensation under the Riot (Damages) Act 1886

7 September 2011

Michael Hayes

The Riot (Damages) Act 1886 is designed to compensate people and businesses which suffer losses following riots. It also enables […]

Third Parties (Rights Against Insurers) Act 2010

26 April 2010

Michael Hayes

The Third Parties (Rights Against Insurers) Act 2010 which received Royal Assent on 25.03.2010 has amended previous legislation governing the […]

Financial Services Act 2010 – class actions removed

Michael Hayes

The Financial Services Act 2010 received Royal Assent on 08.04.2010, being amongst the last few pieces of legislation rushed through […]

Our comments on film finance schemes for the Financial Times

8 March 2010

Michael Hayes

Film finance schemes are back in the news for the wrong reasons, with HMRC investigating claims for tax relief by […]

Financial Services Bill progress

16 February 2010

Michael Hayes

The Financial Services Bill is due to receive its second reading in the House of Lords (when all aspects of […]